For 16 years, Larry Gruber, a fitness coach from Wilton Manors, Florida, received a coupon card to help him pay for a psoriatic arthritis medication he needs that costs more than $7,700 a month.

Each year, Amgen, which makes the drug, called Enbrel, sent the coupon card worth thousands of dollars, and that counted toward Gruber’s health insurance deductible and out-of-pocket maximum.

Using the card, Gruber usually met that maximum by February, leaving his health insurance to fully cover his in-network medical costs and reducing his cost for the drug to $0 for the rest of the year.

But this year, his new health insurer, Oscar HMO of Florida, pocketed the coupon card and required Gruber to pay for the drug until he satisfied the cost-sharing requirements on his own.

If Oscar Health had applied Amgen’s coupon toward Gruber’s cost sharing, he would have been on the hook for about $3,000 in covered services. Without it, he had to use his savings to meet the plan’s $10,600 out-of-pocket maximum.

“The real insult here is that they’re taking the money that’s intended to help you,” said Gruber, who had planned to buy a home next year with his savings. “I feel desperate, pressed against the wall, and squeezed.”

Oscar Health is one of many commercial health insurers that use what are often called copay accumulator programs to keep funds that are meant to defray patients’ out-of-pocket costs for expensive specialty drugs. Over the past decade, more insurers have adopted such strategies to reduce their prescription drug costs, according to Avalere Health, a consulting company.

Patients who rely on copay assistance from drugmakers are typically heavy users of healthcare for whom delays in treatment or worsening conditions can lead to higher costs, according to patient advocates.

Matt Choffin, Florida market president for Oscar Health, did not comment on the specifics of Gruber’s case. He said the company uses copay accumulators to manage rising medical and prescription costs and “to keep monthly premiums as low as possible.”

Drugmakers argue that insurers and pharmacy benefit managers use copay accumulators and other strategies to delay or deny care and steer patients toward medicines that insurers prefer instead. Insurers counter that coupon cards and other patient financial assistance from drug manufacturers drive up premiums and encourage patients to use higher-priced, brand-name drugs instead of less-expensive generics.

Meanwhile, patient advocates say it’s difficult for consumers to find out if their plan uses a copay accumulator or to understand how they work. Not only do the programs make medications unaffordable for consumers, critics argue, but they allow insurers to double-dip.

“They’re collecting the money twice and they’re hurting patients,” said Carl Schmid, executive director of the HIV+Hepatitis Policy Institute, a patient advocacy group.

“Why does it make a difference to Oscar if they get the money from a drug company or, you know, his mother or him?” he said of Gruber’s experience. “They’re still getting the money.”

Controlling Costs or Harming Patients?

Not all insurance types use copay accumulators. Medicare and Medicaid prohibit copay assistance because federal anti-kickback laws forbid drug manufacturers from offering financial incentives to influence patients’ choices. And the Internal Revenue Service prohibits such help for high-deductible plans with health savings accounts. But individual and commercial group plans can use them.

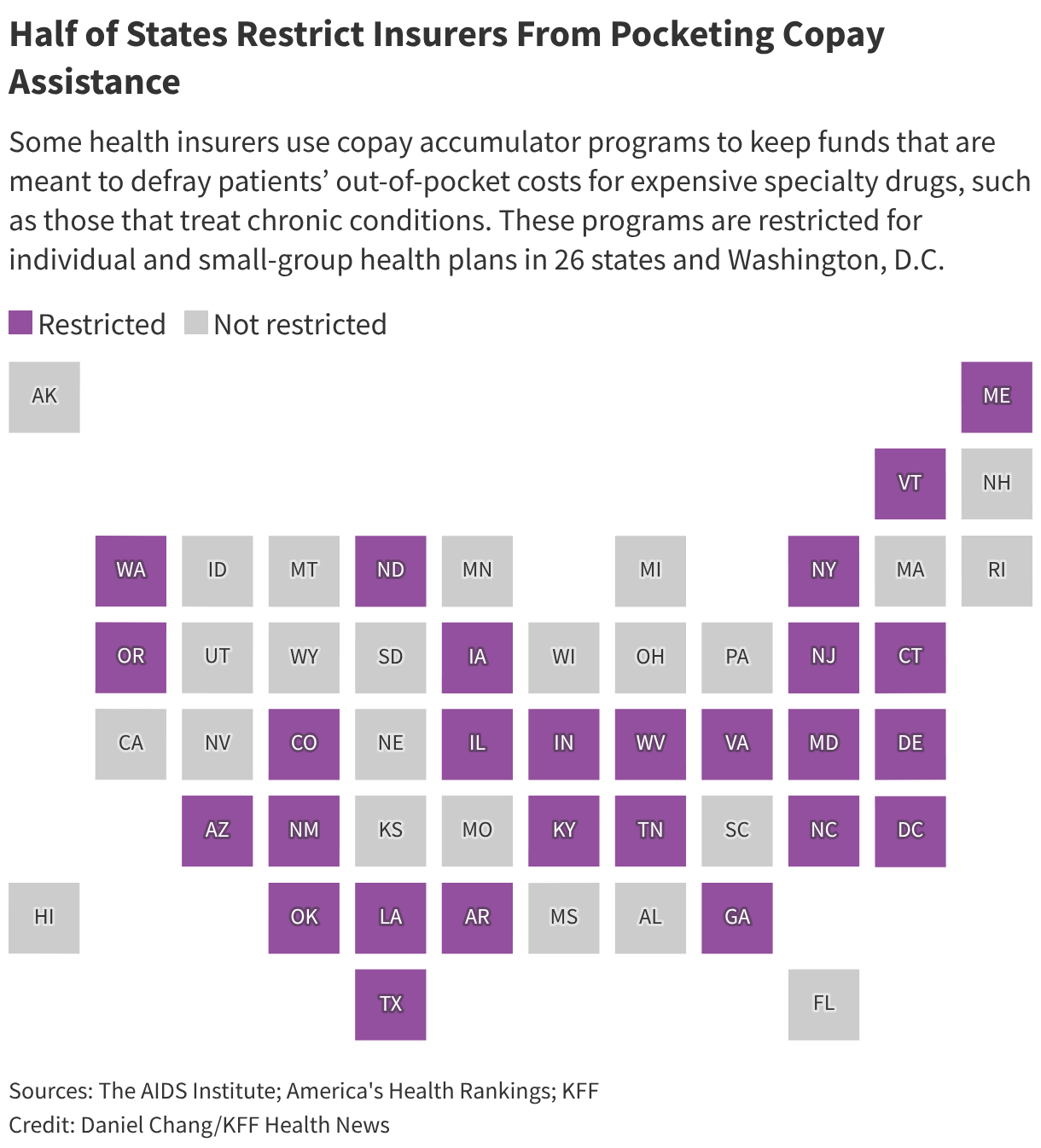

Regulation of copay accumulator programs has fallen largely to states, which oversee individual and small-group plans sold on the Affordable Care Act marketplace.

For 2026, nearly 40% of ACA marketplace plans have such a program, according to a review from The AIDS Institute, a nonprofit group that opposes the programs. Of the 16 insurers that sell plans on the marketplace in Florida, 10 use copay accumulator programs, the review found.

Patients who take brand-name specialty drugs for conditions such as autoimmune disorders, multiple sclerosis, diabetes, HIV, and cancer are most likely to encounter these programs. Health insurers say that making patients share the costs for specialty drugs encourages them to choose value over brand.

But Gruber doesn’t have a choice because there is no medically equivalent generic for Enbrel. Gruber’s livelihood as a trainer depends on his athleticism. The weekly injections, which he has to take for the rest of his life, prevent his joints from getting stiff. When he was diagnosed in 2010, Gruber said, he couldn’t shake hands or lift his knee to get into bed. Without treatment, he said, “I ache from my neck down to my toes.”

If manufacturers priced their drugs affordably, patients like Gruber wouldn’t need financial assistance, said Sean Dickson, a senior vice president for AHIP, a trade association representing insurers.

“Drugmakers offer short-term ‘discounts’ to justify overcharging Americans in the long term, driving up healthcare costs for everyone,” he said in a statement. “Research shows limiting copay coupons can reduce premiums and lower consumers’ out-of-pocket costs.”

Sarah Ryan, a spokesperson for Pharmaceutical Research and Manufacturers of America, a trade association for the pharmaceutical industry, said copay assistance helps patients access medications free of charge or at reduced cost.

“Health insurance is supposed to protect patients,” Ryan said, adding that insurers and pharmacy benefit managers that refuse to count copay assistance toward cost sharing are “leaving patients facing unexpected costs and disrupting their care.”

Insurance companies already have tools to control costs without keeping financial assistance intended for patients, said Rachel Klein, deputy executive director for The AIDS Institute.

Insurers choose what drugs to cover, whether they are medically necessary, and if a patient must try a cheaper alternative first.

“They are the ones making the decisions,” Klein said. “Now the individual is left trying to figure out how they’re going to pay for it.”

Consumers Stuck in the Middle

Before moving to Florida in 2024, Gruber said, he had bought coverage on the ACA marketplaces in Illinois and Louisiana, which prohibit copay accumulators. Gruber said he hadn’t encountered one until his experience with Oscar Health.

He complained to the office of Florida’s insurance consumer advocate, which informed him that the practice is legal in the state and that Oscar Health had disclosed its use of a copay accumulator program. Page 127 of his 168-page evidence of coverage states, “Third party assistance will not count towards your out-of-pocket maximum or deductible.”

Gruber said he selected his coverage using a tool on healthcare.gov that listed all the Florida ACA plans that cover Enbrel. “I always choose the one with the highest deductible to get the lowest premium,” he said, “because I know I’m going to meet it.” His monthly premium is about $315 after subsidies.

Adding to Gruber’s confusion, he said, was that his patient portal with Oscar Health was counting his coupon card at first. He said he met his out-of-pocket maximum in February, and in March Oscar covered all the cost for the medication.

But when he ordered his refill for April, the pharmacy told him that Oscar would cover only $1,000 of the medication’s cost for that month. He would have to pay the remaining $6,700.

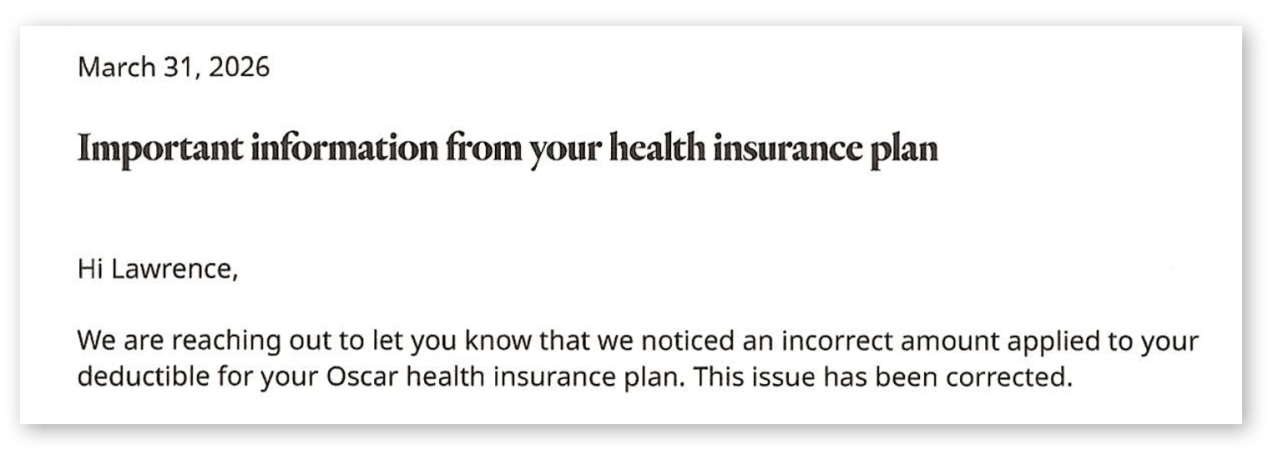

Gruber then received a letter from Oscar Health, telling him that an incorrect amount had been applied to his deductible.

“They sent me a letter that basically stated they made a mistake,” he said. “The fact that they’re allowed to sort of change things midstream is also, I think, a little galling.”

He began rationing the injections, taking them every other week instead of weekly. By May, he had dipped into his savings to pay for the drug.

States Step Up While Federal Oversight Stalls

The first state laws banning copay accumulators were adopted in 2019, and since then more states have moved to regulate the programs, said Gavin Clingham, public policy director for the Alliance for Patient Access, an advocacy group.

“The goal is to build upon that progress at the federal level and to continue to drive this momentum forward,” he said.

Twenty-six states, Washington, D.C., and Puerto Rico have adopted laws banning copay accumulators or prohibiting them for drugs that do not have a generic equivalent. Colorado also prohibits copay accumulators for drugs without a biosimilar. In states that have not banned or restricted the programs, insurance companies decide whether to use them.

But federal regulation of the programs, which would apply to all states, remains at a standstill.

A federal court in 2023 struck down a policy enacted during President Donald Trump’s first term that had permitted insurers to use copay accumulator programs. As a result, the Department of Health and Human Services reverted to an earlier rule that restricts their use to brand-name drugs with a medically appropriate generic equivalent.

After the court ruling, the Biden administration pledged to address copay accumulators in future rulemaking. But HHS has yet to do so, said Schmid, whose group, the HIV+Hepatitis Policy Institute, led a coalition of patient advocacy groups that sued to overturn the rule.

“The Trump administration can stop this once and for all at the national level,” Schmid said. “If they really care about patient affordability, this is something they can do.”

Bipartisan legislation in Congress called the HELP Copays Act would require financial assistance to count toward deductibles and other out-of-pocket costs on plans regulated by the federal government, including much employer-sponsored coverage.

Schmid said the bill has not gotten “enough traction on the Hill yet.”

Other ways to obtain medication don’t help patients facing copay accumulators either. The president’s TrumpRx initiative, an online platform through which consumers can buy prescription drugs at a discount, requires patients to pay out-of-pocket, and the cost does not count toward their plan’s cost-sharing requirements.

Christopher Krepich, a Centers for Medicare & Medicaid Services spokesperson, said that HHS, along with the departments of Labor and the Treasury, intend to address the issue of whether copay assistance must apply toward health plan cost sharing.

Until then, he wrote, “the Departments do not intend to take any enforcement action against health insurance issuers or group health plans based on their treatment of such manufacturer assistance.”

Outside of government regulation, consumers have few protections or alternatives.

Patients who rely on expensive medications — and who have a choice in their health insurance plan — should research their coverage options and choose wisely so they’re not caught by surprise, Clingham said.

That may mean reading plan benefit explanation packages, contacting their state’s insurance regulator, or calling an insurance company to ask if their plans use copay accumulator programs.

For Gruber, the extra expense means he won’t take a vacation this year. He’s also concerned that the money he was saving for a home will now go to his medication costs instead.

“It’s the first thing I think of when I wake up in the morning,” he said. “If this happens every year, it would be financially devastating.”

Are you struggling to afford your health insurance? Have you decided to forgo coverage? Click here to contact KFF Health News and share your story.